Keeping track of your expenses is only one aspect of managing your funds, whether they are for a personal home or a developing business. It necessitates a proactive approach that aids in planning, forecasting, and managing your financial results. One of the most powerful tools for doing exactly that is the budgeted income statement. Before a single dollar is actually generated or spent, this document provides individuals, business owners, and corporate finance teams with a clear picture of what revenues, expenses, and profits are anticipated for a specified future period.

A budgeted income statement is not just a formality. It is a living financial roadmap. When applied properly, it assists companies in matching resources to objectives, spotting possible deficiencies before they become emergencies, and holding departments responsible for meeting budgetary goals. It becomes a compass for those who are passionate about personal finance, pointing them in the direction of disciplined wealth creation and financial independence.

We will go over all you need to know about the budgeted income statement in this thorough tutorial, including its description, components, step-by-step preparation instructions, the distinction between a budget and an actual income statement, and its place in the larger master budgeting process. Additionally, you will learn useful advice and real-world examples that you can implement immediately.

You can also follow us on Facebook and X.com for regular updates on budgeting strategies, financial planning tips, and wealth-building insights.

What Is a Budgeted Income Statement?

A budgeted income statement, sometimes referred to as a projected income statement or pro forma income statement, is a financial record that projects the sales, expenses, and net income of a business or individual for a future time frame, usually a quarter or a fiscal year. The budgeted income statement is completely forward-looking and predicated on planned assumptions, in contrast to the actual income statement, which presents historical facts.

This financial planning tool is a component of the wider master budget, which consists of a number of interrelated budgets, including the cash budget, sales budget, production budget, and direct materials budget. The core of this system is the budgeted income statement, which uses information from several supporting schedules to generate a thorough profitability forecast.

Before the accounting period even starts, business owners and finance managers can set reasonable targets, foresee obstacles, and make data-driven decisions by creating a budgeted income statement early in the planning cycle.

Why Is the Budgeted Income Statement Important?

The Budgeted Income Statement Drives Strategic Decision-Making

Most businesses would function reactively in the absence of a budgeted revenue statement, addressing financial issues only after they have already arisen. Leadership teams may make proactive, strategic decisions all year round with one in place. Before the quarter even starts, management can modify pricing, reduce discretionary expenditure, or step up sales efforts if the anticipated net income falls short of expectations during the budgeting process.

Another important factor in obtaining funding is the budgeted income statement. Businesses are often asked to provide forecasted financial statements to banks, investors, or venture capital organisations. A well-written budgeted income statement shows that management is firmly in control of the company’s financial trajectory and exhibits financial credibility.

Budgeted Income Statement Supports Performance Evaluation

Performance benchmarking is one of the most useful applications of the budgeted income statement. Managers can find variances—areas where the company exceeded or fell short of expectations—by comparing the budgeted and actual outcomes at the conclusion of the term. A key component of good financial management and ongoing development is this budget-versus-actual review.

The same holds true for people who use a personal budgeted income statement. You may improve your financial awareness and make quick course corrections by comparing your monthly projected income and expenses to actual results.

Key Components of a Budgeted Income Statement

Budgeted Revenues: The Foundation of the Budgeted Income Statement

Projected revenues, or the total revenue anticipated from sales of products or services over the forecast period, are always the first item on the budgeted income statement. The sales budget, which projects unit sales volumes and anticipated selling prices, is usually the source of this number.

Revenues can be broken down by segment for companies with several product lines or service categories to give a more accurate and thorough view. Since accurate revenue forecasting depends on pricing plans, market conditions, competitive dynamics, and historical trends, it is perhaps the most difficult aspect of creating a planned income statement.

Revenue Assumptions and Inputs

Take into account the following inputs when creating the revenue part of your planned income statement:

- Prior year actual revenues and growth trends

- Planned price changes or product launches

- Expected market share shifts

- Seasonal demand patterns

- Economic outlook and consumer confidence indicators

Budgeted Cost of Goods Sold (COGS)

The cost of goods sold, or the direct costs of manufacturing the goods or services sold during the period, is shown below revenues in the budgeted income statement. The production budget, as well as the direct labour and material costs, are usually the sources of COGS.

The cost of providing services, including direct labour, supplies, and subcontractor fees, may be shown in this area for service businesses. Maintaining a healthy gross profit margin on your budgeted revenue statement requires strict control over COGS.

Gross Profit in the Budgeted Income Statement

Budgeted COGS is subtracted from budgeted revenues to determine gross profit. Because it shows the company’s core profitability before overhead and administrative expenses are taken into account, it is one of the most significant measures on the planned income statement.

Improved operational efficiency is indicated by a growing gross profit margin across subsequent planned income statements. A decreasing margin indicates that pricing power is eroding or that cost constraints are increasing.

Budgeted Operating Expenses

The overhead costs necessary to operate the business that are not directly related to production are referred to as operating expenses. Usually, these consist of:

- Selling expenses — advertising, commissions, marketing campaigns, trade show costs

- General and administrative expenses — salaries for administrative staff, office rent, insurance, legal fees, and technology costs

- Research and development — for product-driven companies investing in innovation

- Depreciation and amortization — non-cash charges that reduce the book value of assets over time

The selling expense budget and the general and administrative expense budget, which are sub-components of the master budget, are used to estimate each of these categories on a budgeted income statement.

Budgeted Operating Income (EBIT)

The budgeted income statement shows operating income, commonly referred to as earnings before interest and taxes, or EBIT, after subtracting all operating costs from gross profit. Regardless of funding choices or tax responsibilities, this figure illustrates the anticipated profitability of the main business operations.

Interest and Other Non-Operating Items

Interest income, interest expense, and other non-operating gains or losses are also included in the budgeted income statement. These things are especially crucial for companies with large debt loads or huge cash and investment holdings.

Budgeted Net Income: The Bottom Line

The budgeted income statement determines net income, or the “bottom line,” after deducting taxes using the business’s expected effective tax rate. Among all the figures in the document, this one is the most closely followed. The profit that the company anticipates giving to its shareholders or keeping for internal business reinvestment is represented by budgeted net income.

When it comes to personal finance applications, net income on a budgeted income statement refers to your anticipated monthly or annual surplus, or the amount of money you anticipate having left over after all of your scheduled sources of income and costs are taken into consideration.

How to Prepare a Budgeted Income Statement: Step-by-Step

Step 1: Start with the Sales Budget

Forecasting sales is always the first step in creating a budgeted income statement. Collect information from your sales team, examine past patterns, account for any upcoming marketing campaigns, and set reasonable revenue goals for every product or service category.

Step 2: Build the Cost of Goods Sold Budget

Determine the cost of delivering the predicted sales by working backward. To determine the anticipated COGS on your budgeted income statement, extract information from your production, direct materials, and direct labour budgets.

Step 3: Calculate Gross Profit

To calculate gross profit, deduct planned COGS from budgeted revenues. To make sure your forecasted income statement accurately depicts operational efficiency, compare the resulting margin to previous periods and industry norms.

Step 4: Estimate Operating Expenses

Go through each item of operating expenses in a methodical manner. To determine your operating expense forecasts for the budgeted income statement, use either incremental budgeting (modifying previous year data) or zero-based budgeting (rebuilding each item from begin).

Step 5: Compute Operating Income

operational income is calculated by deducting all operational costs from gross profit. On your budgeted income statement, this provides you with a clear image of how profitable your main business should be.

Step 6: Factor In Interest and Taxes

Non-operating items like interest income and expenses might be added or subtracted. Next, compute the projected tax provision by applying your estimated effective tax rate to pre-tax income. Your expected net income, which is the last amount on the budgeted income statement, is the outcome.

Step 7: Review, Stress-Test, and Revise

Model best-case, worst-case, and base-case situations to stress-test your budgeted income statement before finalising it. In addition to preparing the organization for uncertainty, this aids leadership in comprehending the variety of possible outcomes.

Budgeted Income Statement vs. Actual Income Statement

The differential between an actual income statement and a budgeted income statement is one of the most crucial ones in financial management. The budgeted version reflects what is planned and is therefore prospective. The real version documents what transpired; it is retrospective.

Finance teams can find discrepancies and comprehend why actual results deviate from projections by routinely comparing these two documents. When actual revenues surpass budget or actual expenses fall short of budget, favourable variations take place. When revenues are insufficient or expenses exceed budget, unfavourable deviations take place.

Budgeting becomes a continuous cycle of planning, monitoring, and modification when a planned income statement is regularly compared against actuals. High-performing companies all across the world are increasingly implementing what is commonly known as rolling forecast management.

Budgeted Income Statement and the Master Budget

The budgeted income statement is not a stand-alone document. It is the result of a thorough master budget that connects all of an organization’s financial and operational goals. Usually, the master budget consists of:

- Sales budget

- Production budget

- Direct materials budget

- Direct labor budget

- Manufacturing overhead budget

- Selling and administrative expense budget

- Budgeted income statement

- Cash budget

- Budgeted balance sheet

Each of these elements ensures that all assumptions are internally consistent by feeding into the budgeted income statement. For instance, COGS on the budgeted income statement is directly impacted by the production budget, which establishes the quantity of products produced. The marketing expenditure that shows up under operating expenses is determined by the selling expense budget.

Anyone working in business finance, managerial accounting, or corporate financial planning must comprehend how the budgeted income statement fits into the master budget structure.

Portfolio Budget Statement: A Related Concept You Should Know

If you have been exploring financial planning tools on Wealth Start Today, you may have come across our previously published article on the Portfolio Budget Statement — a closely related yet distinct financial document. While the budgeted income statement focuses on projected revenues, expenses, and net income for a business or household over a specific period, the Portfolio Budget Statement takes a broader view. It encompasses the allocation and management of financial assets across various investment categories — such as stocks, bonds, real estate, and cash equivalents — within the context of an overall wealth-building strategy.

The Portfolio Budget Statement is particularly valuable for investors and high-net-worth individuals who need to align their investment income projections with their overall income and expense budgets. When used alongside a budgeted income statement, the Portfolio Budget Statement provides a 360-degree view of both operational income and investment returns — giving you the most complete financial picture possible. Together, these two tools form a powerful combination for anyone serious about taking control of their financial future.

Common Mistakes to Avoid When Creating a Budgeted Income Statement

Overestimating Revenue on Your Budgeted Income Statement

Unrealistic revenue forecasting is one of the most common and detrimental mistakes made while creating a budgeted income statement. Inflated profit expectations and bad operational choices, such recruiting too quickly or committing to excessive capital expenditures, result from overly optimistic sales estimates. Your revenue estimates should always be supported by reliable historical data, market analysis, and cautious growth projections.

Ignoring Seasonality in the Budgeted Income Statement

Throughout the year, a lot of firms have large swings in their revenue and expenses. Inaccurate monthly or quarterly estimates will result from a budgeted income statement that does not take seasonality into consideration. When necessary, apply seasonal adjustment variables to your annual budget by breaking it down by time.

Failing to Involve Key Stakeholders

Without input from sales, operations, and department heads, a budgeted revenue statement created only by the finance team is unlikely to accurately represent the business’s realities. Stronger organisational buy-in and more accurate projections are the results of inclusive budgeting, in which every department contributes to the numbers that will eventually appear on the planned income statement.

Treating the Budgeted Income Statement as Static

The corporate environment is always evolving. If there have been significant changes in the market, supply chain interruptions, or competitive developments, a budgeted revenue statement created in January can be somewhat outdated by April. Best-practice companies use rolling projections to update their budgeted income statement on a frequent basis, treating it as a dynamic document.

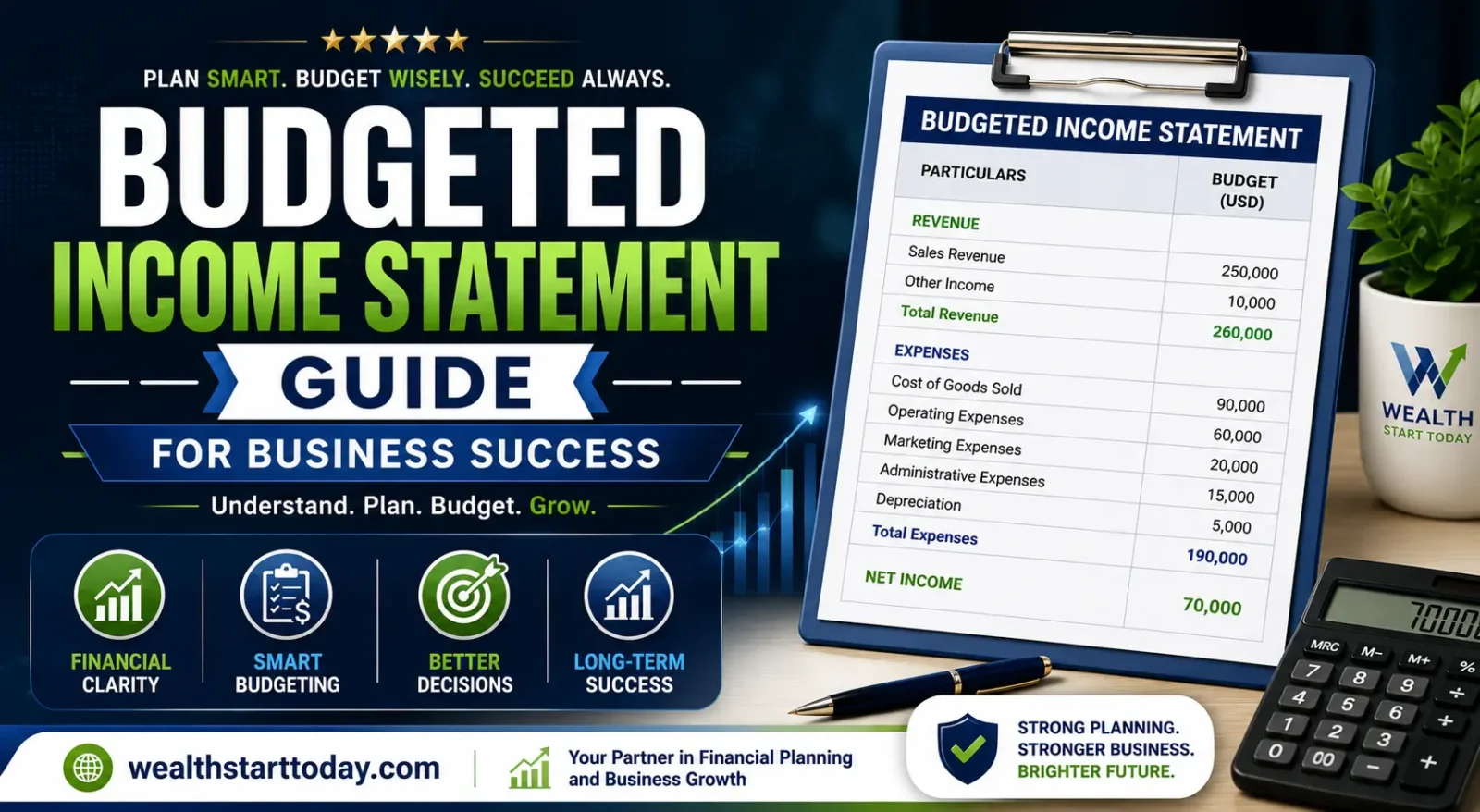

Real-World Example of a Budgeted Income Statement

Here is a condensed budgeted income statement for a small product-based business for the fiscal year to help visualise this idea:

| Line Item | Budgeted Amount |

|---|---|

| Net Sales Revenue | $2,500,000 |

| Cost of Goods Sold | ($1,400,000) |

| Gross Profit | $1,100,000 |

| Selling Expenses | ($250,000) |

| General & Admin Expenses | ($180,000) |

| Depreciation | ($70,000) |

| Total Operating Expenses | ($500,000) |

| Operating Income (EBIT) | $600,000 |

| Interest Expense | ($40,000) |

| Pre-Tax Income | $560,000 |

| Income Tax (25%) | ($140,000) |

| Budgeted Net Income | $420,000 |

This example shows how the budgeted income statement’s lines logically flow from revenues to net income, with a distinct division between operational income, gross profit, and the bottom line.

How Wealth Start Today Helps You Master Budgeting

At Wealth Start Today, our mission is to empower individuals, families, and small business owners with the financial knowledge and tools they need to build lasting wealth. Wealth Start Today’s Budgeting category is packed with in-depth guides, practical templates, and expert strategies covering everything from personal cash flow management to advanced business budgeting techniques — including how to prepare and use a budgeted income statement effectively.

Whether you are just starting your financial journey or looking to sharpen your existing money management skills, Wealth Start Today is your trusted resource for clear, actionable, and authoritative financial guidance. We consider financial literacy to be the cornerstone of freedom rather than a luxury. One of the most significant things you can do to achieve that independence is to become proficient with tools like the budgeted income statement.

FAQs About the Budgeted Income Statement

Q1: What is the main purpose of a budgeted income statement?

Projecting a company’s or individual’s anticipated revenues, costs, and net income for a future period is the primary goal of a planned income statement. Throughout the budgetary term, it acts as a financial road map that directs resource allocation, planning, and performance evaluation.

Q2: How is a budgeted income statement different from an actual income statement?

An actual income statement presents the actual historical results for a finished accounting period, whereas a budgeted income statement is forward-looking and predicated on planned assumptions. Managers can find and examine financial differences by comparing the two.

Q3: What are the main components of a budgeted income statement?

Projected revenues, cost of products sold, gross profit, operating expenditures (administrative and selling), operating income, interest and other non-operating items, income taxes, and planned net income are the main elements of a budgeted income statement.

Q4: How often should a business update its budgeted income statement?

The budgeted income statement should be reviewed and updated at least once every quarter. Rolling forecasts are frequently used by high-performing companies to revise their projections on a monthly basis, taking into account the most recent assumptions and business realities.

Q5: Can individuals use a budgeted income statement for personal finance?

Of course. By projecting all anticipated income streams (salary, investments, freelance income) and all planned expenses (rent, food, insurance, savings contributions) for a future time, people can apply the budgeted income statement concept to personal finance. As a result, a personal financial projection is produced that encourages prudent money management.

Q6: What is the relationship between the budgeted income statement and the master budget?

One important result of the master budget is the budgeted income statement. A single projected profitability statement for the budget period is created by combining data from supporting budgets, such as the operating expense, production, and sales budgets.

Q7: What is a common mistake when preparing a budgeted income statement?

Overestimating revenues is the most frequent error. Overly optimistic sales forecasts might result in bad operational choices and inflated predicted profitability. Forecasts of revenue should always be based on data-driven, realistic assumptions, and you should think about modelling several possibilities on your budgeted income statement.

Conclusion

The budgeted income statement is one of the most essential tools in the arsenal of any financially disciplined individual, small business owner, or corporate finance professional. It turns budgeting from a passive record-keeping activity into a dynamic, strategic planning process by predicting revenues, costs, and net income prior to the start of a financial term.

From understanding its core components to learning how to prepare one step by step, from avoiding common pitfalls to integrating it within the master budget framework — mastering the budgeted income statement gives you genuine control over your financial destiny. Whether you are steering a multimillion-dollar enterprise or managing a household budget, the principles behind the budgeted income statement are universally applicable and powerfully effective.

At Wealth Start Today, we are committed to bringing you the most comprehensive, authoritative, and trustworthy financial content available. Explore our full Budgeting section to discover more guides and strategies that can help you plan smarter, spend wiser, and build wealth faster.

Follow us on Facebook and X.com to join a community of financially empowered individuals who are committed to taking control of their money — starting today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment